Market Review: Black Tuesday Triggers Dual Circuit Breakers and Systemic Liquidations

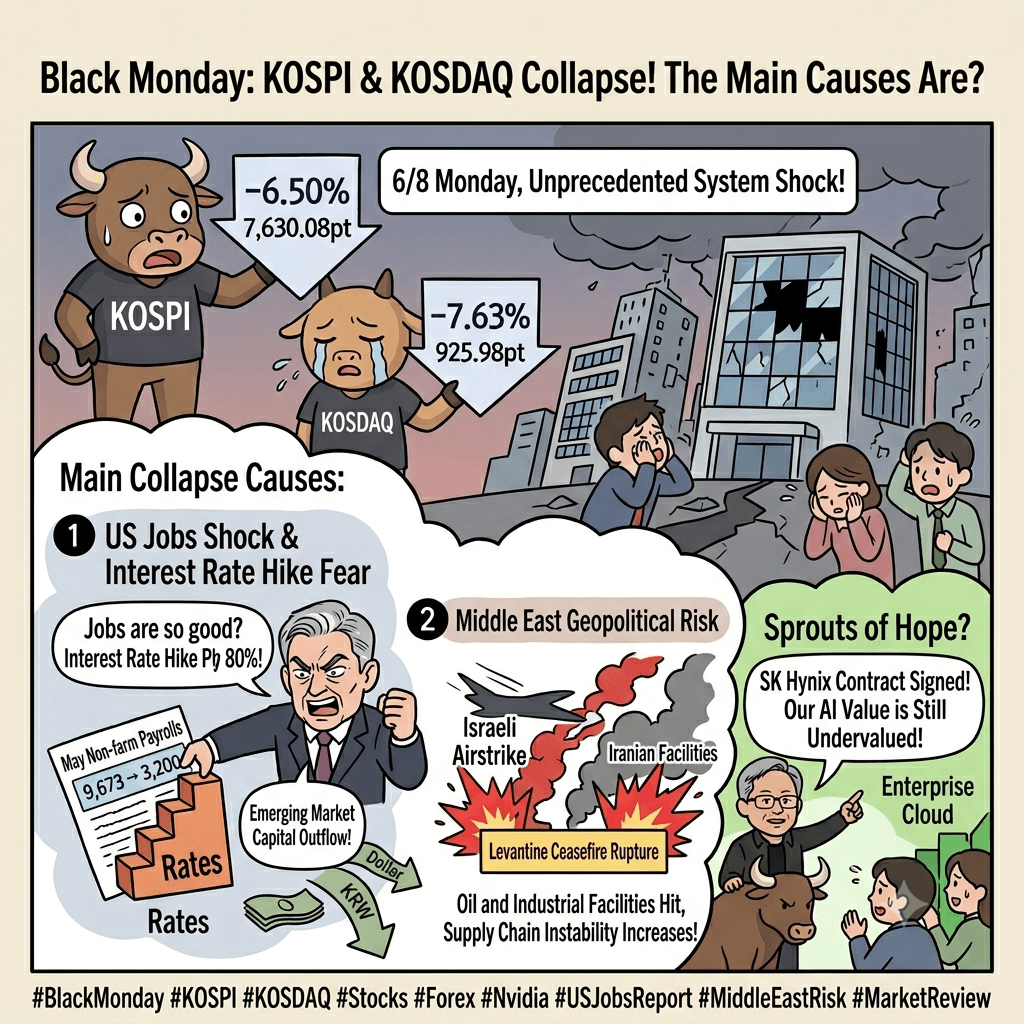

The domestic financial markets endured an unprecedented systemic shock on Monday, June 8, 2026, culminating in one of the most violent structural liquidations in modern exchange history.

Panic selling quickly overwhelmed the trading floor, triggering a KOSPI Circuit Breaker during the morning session and a KOSDAQ Selling Sidecar/Circuit Breaker by the afternoon. The benchmark KOSPI closed with a devastating -6.50% loss at 7,630.08pt after sinking as low as Client-Low 7,442pt. Meanwhile, the junior KOSDAQ collapsed by -7.63% to close at 925.98pt, completely erasing its entire performance build-up to plunge into negative territory year-to-date.

The driving force behind this severe capitulation was an unhedged macro exit. Foreign institutional allocators offloaded over 1.18 trillion KRW in net KOSPI spot equities, focusing their automated liquidations heavily inside over-leveraged tech hardware, automotive chains, and core machinery.

The downward spiral accelerated drastically during late-afternoon trading as domestic financial investment desks and institutional algos pulled buy orders entirely, letting mandatory margin calls, stock loans, and CFD liquidations trigger a blind cascade across the secondary boards.

1. The Macro Backdrop: The Non-Farm Payroll Shock and Renewed Iranian Infrastructure Flares

The international macroeconomic landscape simultaneously delivered multiple tail-risk catalysts, sparking a coordinated global flight from emerging market assets:

- The Robust US Jobs Print & The 80% Rate Hike Probability: The primary monetary shock was triggered by the US May Non-Farm Payrolls data, which surged far past consensus forecasts at 172,000 new jobs. The resilient labor metric completely dismantled near-term easing expectations, with global swap desks rapidly pricing in an astronomical 80% mathematical probability of an imminent Federal Reserve interest rate hike. Instantly, the US 10-Year Treasury yield surged past the critical 4.5% ceiling, triggering swift global liquidity evacuations from emerging market growth equities.

- The Levantine Ceasefire Rupture: Geopolitical tensions exploded following a surprise Israeli air assault targeting premium Iranian petrochemical and industrial facilities. Executed immediately after Donald Trump hinted at a potential mid-June armistice roadmap, the strategic offensive confirmed that localized factions are structurally avoiding immediate diplomacy. The risk of widespread infrastructure destruction across the Middle East triggered sharp energy anxieties, heavily clamping buy-side conviction across energy-importing Asian manufacturing economies.

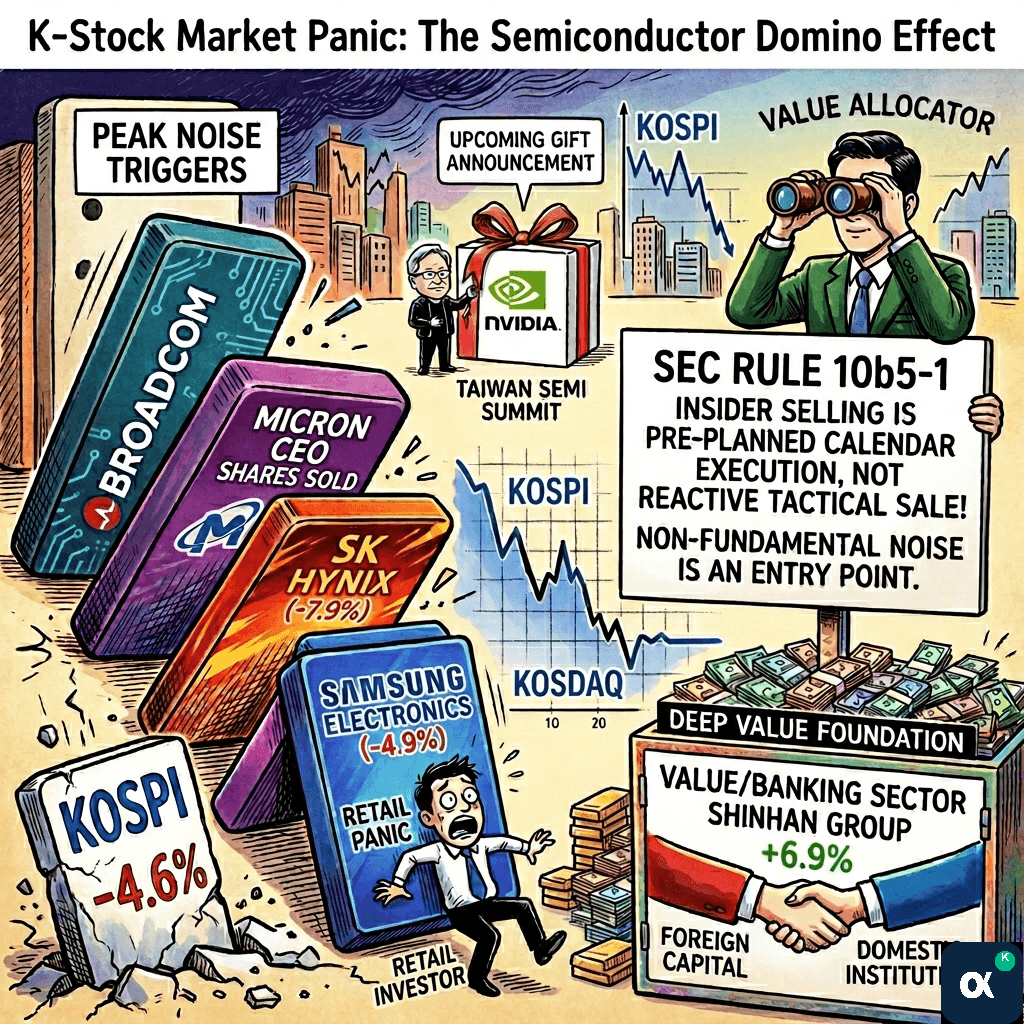

2. The Structural Catalyst Complex: Pandemic-Depth Semiconductor Routs and the Margin Cascade

The localized technical breakdown was severely exacerbated by international tech hardware liquidations and severe mechanical margin liquidations underneath the domestic surface:

The -10% Philadelphia Semiconductor Capitulation

Sovereign domestic technology sentiment was directly unhinged by a historic overnight collapse in the Philadelphia Semiconductor Index, which recorded a jaw-dropping -10% rout—its steepest single-day decline since the pandemic panic of March 2020. Severe valuation adjustments across tier-1 names like Micron (-13.3%) and Intel (-11.3%), compounded by Broadcom’s recent conservative guidance and imminent capital diversions surrounding the highly anticipated SpaceX IPO, triggered systematic, indiscriminate index-weight selling across correlated Asian tech giants.

The Margin Call Exhaustion Floor

With the KOSDAQ index registering severe declines in seven out of the last eight sessions, the absolute absence of an immediate structural stabilization framework from financial regulators left the secondary board defenseless. The afternoon slide was heavily amplified by automated liquidation loops. As asset prices broke near-term technical support boundaries, thousands of retail accounts instantly faced automated margin liquidations through stock-option loans and contract-for-difference (CFD) vehicles, creating a vertical, non-fundamental dumping wave that disconnected entirely from corporate fundamentals.

3. High-Conviction Structural Themes: The Jensen Huang Shield vs. The Absolute Value Rotations

Despite the overwhelming index-wide selling pressure, a vital fundamental divergence emerged around specific enterprise networks and localized technology shields:

The Jensen Huang ‘Undervaluated’ Declaration

Nvidia CEO Jensen Huang aggressively utilized his physical presence in Seoul to mount a robust structural defense of the local supply ecosystem. Formally declaring that domestic artificial intelligence components are trading at "extremely undervalued" valuation multiples, the executive officially confirmed the execution of a binding 2-year supply treaty with SK Hynix, with explicit provisions for long-term strategic extensions. This definitive corporate anchor injected massive structural confidence, allowing premium hardware leaders to recoup up to half of their intraday losses off their absolute technical floors.

The Enterprise Cloud and Telecom Safe Havens

Capital fleeing vulnerable growth segments sought refuge inside defensive corporate ecosystems that directly capitalized on the physical presence of Nvidia’s leadership team. Select instruments leveraging deep localized enterprise AI transformations or commanding defensive domestic cash flows stood out as rare green pockets amidst a completely red market landscape.

K-Stock Radar & ETF Watch: Today’s High-Conviction Seven

The following single-point interactive tracker monitors the seven core instruments currently commanding the exchange’s absolute liquidity, policy backings, and thematic momentum.

<iframe src="https://radar.korean-stocks.com/widget?tickers=005930,000660,035420,011210,017670,0193W0,455850&embed=true" width="100%" height="430" style="border:none;border-radius:12px;" loading="lazy" title="K-Stock Radar"></iframe>

1. Samsung Electronics (005930)

Sustained an intensive -8.1% hit as multi-billion dollar foreign index baskets automatically reduced equity weights. The stock bore the brunt of the global semiconductor re-rating despite maintaining stellar localized yield metrics.

2. SK Hynix (000660)

Demonstrated exceptional relative resilience to limit its decline to -4.4%. The asset was aggressively anchored by Jensen Huang’s formal confirmation of a multi-year HBM binding supply treaty, rebounding violently from its technical maximum draw-down floor of -23%.

3. NAVER (035420)

Staged an extraordinary +11.7% counter-cyclical breakout. Insatiable buy-side demand flooded its order book following high-level corporate confirmations of its direct physical AI integration framework during Jensen Huang’s summit tour of its advanced 1784 infrastructure.

4. SK Networks (011210)

Locked into a maximum +30.0% daily limit-up configuration. The asset captured extreme speculative and institutional capital as a primary beneficiary of localized data-center asset transformations and expanding infrastructure alliances aligned with international tech leadership.

5. SK Telecom (017670)

Closed in positive territory up +2.3%, validating its structural status as an elite defensive safe haven. Benefiting from sticky consumer subscription cash flows and zero exposure to global manufacturing margins, it absorbed substantial defensive institutional inflows.

6. KODEX Samsung Electronics Single-Stock Leverage (0193W0)

Operated as the absolute focal point of programmatic trading volume. Amplifying the massive vertical swing of the underlying asset, this high-beta vehicle experienced intense liquidations before catching a late-afternoon bounce off index-support levels.

7. SOL AI Semiconductor Materials, Parts & Equipment ETF (455850)

Faced intense structural turbulence as index-driven selling dragged down premium equipment components. However, as underlying earnings targets for core packaging and fabrication networks remain untouched by global analysts, it continues to position at an extreme historical value discount.

<blockquote>

Strategic Summary: The catastrophic dual Circuit Breakers on the KOSPI and KOSDAQ represent a classic macro-driven forced liquidation event rather than an organic corporate decay cycle. With trailing consensus earnings targets for premier semiconductor lines completely untouched, and given that SK Hynix’s vertical correction accurately halted at its historical -23% maximum cyclical drawdown corridor, the current panic marks a generational technical displacement window.

- Actionable Tactical Vectors:

- The Institutional Anchor Re-build: Avoid participating in forced panic sales during localized margin-call windows. Systematically utilize this deep index-wide distress to rebuild structural positioning inside elite memory leaders and physical AI beneficiaries like SK Hynix and NAVER, which are directly insulated by binding multi-year treaties and concrete corporate catalysts.

- The Defensive Telecom & Cloud Sleeve: Maintain a sturdy defensive cash-flow sleeve inside sovereign network operators and enterprise holding platforms. As international macro yields adjust to sticky US inflation and shifting geopolitical boundaries ahead of upcoming MSCI reviews, these low-beta infrastructure plays provide invaluable valuation protection and critical structural support.

</blockquote>

Leave a Reply